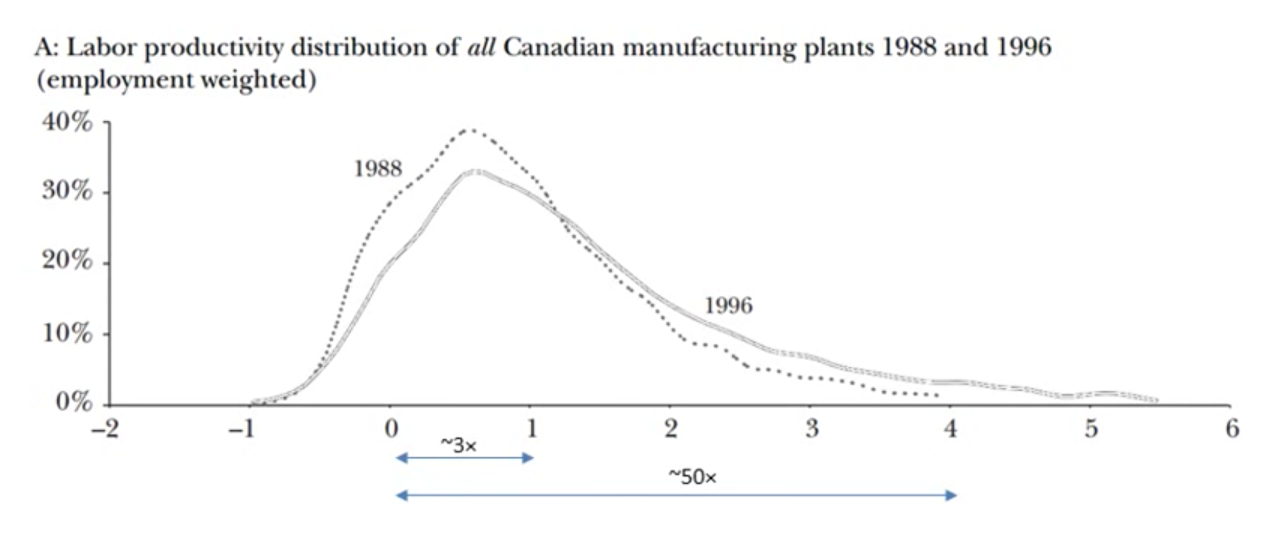

class: title-slide # 1.12 — New Trade Theory II ## ECON 324 • International Trade • Spring 2023 ### Ryan Safner<br> Associate Professor of Economics <br> <a href="mailto:safner@hood.edu"><i class="fa fa-paper-plane fa-fw"></i>safner@hood.edu</a> <br> <a href="https://github.com/ryansafner/tradeS23"><i class="fa fa-github fa-fw"></i>ryansafner/tradeS23</a><br> <a href="https://tradeS23.classes.ryansafner.com"> <i class="fa fa-globe fa-fw"></i>tradeS23.classes.ryansafner.com</a><br> --- class: inverse # Outline ### [Increasing Returns](#3) ### [Trade and Variety](#14) ### [Monopolistic Competition](#14) --- class: inverse, center, middle # Increasing Returns --- # PPF: Decreasing Costs .pull-left[ - Increasing returns `\(\iff\)` decreasing costs - PPF is *convex* to origin - .hi[Marginal rate of transformation (MRT)] .hi-purple[*decreases*] as we produce more of a good - Again: .b[“slope”], .b[“relative price of x”], .b[“opportunity cost of x”] - Amount of y given up to get 1 more x ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-1-1.png" width="504" style="display: block; margin: auto;" /> ] --- # PPF: Decreasing Costs .pull-left[ - To simplify our graph, assume .blue[Home] and .red[Foreign] have identical preferences (same indifference curve), and identical endowments (both start at A) ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-2-1.png" width="504" style="display: block; margin: auto;" /> ] --- # PPF: Decreasing Costs .pull-left[ - Countries open up trade, face same relative prices - Each country exploits economies of scale, producing only one good - .blue[Home] produces x, .red[Foreign] produces y - Points B and B' ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-3-1.png" width="504" style="display: block; margin: auto;" /> ] --- # PPF: Decreasing Costs .pull-left[ - Countries open up trade, face same relative prices - Each country exploits economies of scale, producing only one good - .blue[Home] produces x, .red[Foreign] produces y - Points B and B' - Trade and reach a higher indifference curve at C ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-4-1.png" width="504" style="display: block; margin: auto;" /> ] --- # PPF: Decreasing Costs .pull-left[ - Countries open up trade, face same relative prices - Each country exploits economies of scale, producing only one good - .blue[Home] produces x, .red[Foreign] produces y - Points B and B' - Trade and reach a higher indifference curve at C ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-5-1.png" width="504" style="display: block; margin: auto;" /> ] --- # PPF: Decreasing Costs .pull-left[ - Countries open up trade, face same relative prices - Each country exploits economies of scale, producing only one good - .blue[Home] produces x, .red[Foreign] produces y - Points B and B' - Trade and reach a higher indifference curve at C ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-6-1.png" width="504" style="display: block; margin: auto;" /> ] --- # (Anti-)Competitive Implications of Economies of Scale .pull-left[ ### .hi-blue[U.S.] <img src="1.12-slides_files/figure-html/unnamed-chunk-7-1.png" width="504" style="display: block; margin: auto;" /> ] .pull-right[ ### .hi-red[China] <img src="1.12-slides_files/figure-html/unnamed-chunk-8-1.png" width="504" style="display: block; margin: auto;" /> ] .smallest[ - Before trade, China has lower `\(AC\)` and `\(p\)` than U.S. ] --- # (Anti-)Competitive Implications of Economies of Scale .pull-left[ - Trade increases demand for China’s output - Lowers `\(AC\)` and `\(p\)` even further, further outcompeting U.S. ] .pull-right[ ### .hi-red[China] <img src="1.12-slides_files/figure-html/unnamed-chunk-9-1.png" width="504" style="display: block; margin: auto;" /> ] --- # (Anti-)Competitive Implications of Economies of Scale .pull-left[ - Suppose .hi-orange[Vietnam] actually has lower `\(AC\)` than .hi-red[China], once it gets up to scale (V1) - Chinese economies of scale have world market price at C - Current market price provides no profit to Vietnamese producers starting production at V0 - World is .hi-purple[inefficiently “locked in”] to Chinese production, .hi-purple[sub-optimal path dependence] ] .pull-right[ ### .hi-red[China] and .hi-orange[Vietnam] <img src="1.12-slides_files/figure-html/unnamed-chunk-10-1.png" width="504" style="display: block; margin: auto;" /> ] --- # (Anti-)Competitive Implications of Economies of Scale .pull-left[ - .b[Policy implication for Vietnam]: shut out imports from China with tariffs, and subsidize this industry to get it up to scale - In the long run, Vietnam can become the least-cost producer, increasing welfare ] .pull-right[ ### .hi-red[China] and .hi-orange[Vietnam] <img src="1.12-slides_files/figure-html/unnamed-chunk-11-1.png" width="504" style="display: block; margin: auto;" /> ] --- class: inverse, center, middle # Trade and Variety --- # Trade and Variety .pull-left[ - Consumers are better off with more variety - Two interpretations of why: 1. .hi-purple[Love of variety]: consumers value variety for its own sake (directly enters utility function) 2. .hi-purple[Ideal variety]: consumers have an ideal variety in mind, and having more varieties available increases probability that each consumer matches with their ideal variety ] .pull-right[ .center[  ] ] --- # Trade & Variety: Tradeoff Between Variety & Cost .pull-left[ - Why can’t consumers each always have their favorite variety? - Tradeoff between variety and (average) cost ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-12-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Trade & Variety: Tradeoff Between Variety & Cost .pull-left[ - Why can’t consumers each always have their favorite variety? - Tradeoff between variety and (average) cost - If every consumer had their favorite variety: many varieties, each firm produces very few units at a very high price `\((Q_M, P_M)\)` ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-13-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Trade & Variety: Tradeoff Between Variety & Cost .pull-left[ - Why can’t consumers each always have their favorite variety? - Tradeoff between variety and (average) cost - If every consumer had their favorite variety: many varieties, each firm produces very few units at a very high price `\((Q_M, P_M)\)` - If there are only a few varieties, few firms produce many units at very low price `\((Q_F, P_F)\)` ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-14-1.png" width="504" style="display: block; margin: auto;" /> ] --- # International Trade and Variety .pull-left[ .content-box-green[ .hi-green[Example] - Suppose it takes 2 workers to design a motorcyle - Once designed, it takes 1 worker to produce a motorcycle - There are 2 countries, each with 10 workers ] ] .pull-right[ .center[ Without trade, in each country:  8 units of 1 variety ] ] --- # International Trade and Variety .pull-left[ .content-box-green[ .hi-green[Example] - Suppose it takes 2 workers to design a motorcyle - Once designed, it takes 1 worker to produce a motorcycle - There are 2 countries, each with 10 workers ] ] .pull-right[ .center[ Alternatively:  3 units each of 2 varieties ] ] --- # International Trade and Variety .pull-left[ .content-box-green[ .hi-green[Example] - Suppose it takes 2 workers to design a motorcyle - Once designed, it takes 1 worker to produce a motorcycle - There are 2 countries, each with 10 workers ] ] .pull-right[ .center[ With trade:   Each country specializes in one variety ] ] --- # International Trade and Variety .pull-left[ .content-box-green[ .hi-green[Example] - Suppose it takes 2 workers to design a motorcyle - Once designed, it takes 1 worker to produce a motorcycle - There are 2 countries, each with 10 workers ] ] .pull-right[ .center[ With trade:  Each country specializes in one variety ] ] --- # International Trade and Variety .pull-left[ .content-box-green[ .hi-green[Example] - Suppose it takes 2 workers to design a motorcyle - Once designed, it takes 1 worker to produce a motorcycle - There are 2 countries, each with 10 workers ] - Suppose they trade 4 Harleys for 4 Kawasakis ] .pull-right[ .center[ With trade:  Each country ends up with 4 units of 2 varieties ] ] --- # International Trade and Variety .pull-left[ - Globalization reduces geographic variation (more places look the same, have same amenities) - But increases varieties available to individuals in each area ] .pull-right[ .center[   .quitesmall[ A McDonalds in China, and a Chinese restaurant in the U.S. ] ] ] --- class: inverse, center, middle # Monopolistic Competition --- # The Role of the Firm in Trade .pull-left[ .smaller[ - Classical trade theory (Ricardo, Hecksher-Ohlin, etc) has no role for the firm! - might as well be people directly selling wheat or computers, etc. - Once we jettison the unrealistic assumption of perfect competition `\((p=MC)\)`, we can say a lot more about firms and trade - We move to a theory of .hi[imperfect competition]: where firms have market power (but not full market power, as in a monopoly) ] ] .pull-right[ .center[  ] ] --- # Imperfect Competition .center[  ] --- # Imperfect Competition .center[  ] --- # Imperfect Competition .center[  ] --- # Imperfect Competition .center[  ] --- class: inverse, center, middle # Monopolistic Competition --- # Monopolistic Competition .pull-left[ - .hi[Monopolistic competition]: **each firm has _some_ market power**, but, the industry has .hi-purple[free entry and exit] (**no barriers to entry**) - Each firm faces its own downward-sloping demand - Firms are price-searchers - Model as a hybrid of monopoly and perfect competition models ] .pull-right[ .center[  ] ] --- # Monopolistic Competition: Product Differentiation .pull-left[ - .hi[Product differentiation]: firms’ products are .hi-purple[imperfect substitutes] - Consumers recognize **non-price differences** between sellers’ goods - Brand name & reputation - Customer service - Product features, shape, color, etc. - Marketing - Location, convenience ] .pull-right[ .center[  ] ] --- # Monopolistic Competition: Residual Demand .pull-left[ .smallest[ - Each firm faces own downward-sloping .hi-blue[“residual” demand] for each firm’s products - Firm faces market demand (for broad product) *leftover* from all other firms’ sales - .hi-green[Example]: demand for *Lenovo* laptops `\(\approx\)` demand for *laptops* minus laptops supplied by Acer, Asus, Apple, Dell, etc. ] ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-15-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Monopolistic Competition Model: Short Run .pull-left[ <img src="1.12-slides_files/figure-html/unnamed-chunk-16-1.png" width="504" style="display: block; margin: auto;" /> ] .pull-right[ - **Short Run**: model firm as a price-searching monopolist: ] --- # Monopolistic Competition Model: Short Run .pull-left[ <img src="1.12-slides_files/figure-html/unnamed-chunk-17-1.png" width="504" style="display: block; margin: auto;" /> ] .pull-right[ - **Short Run**: model firm as a price-searching monopolist: - `\(q^*\)`: where `\(\color{purple}{MR(q)}=\color{red}{MC(q)}\)` ] --- # Monopolistic Competition Model: Short Run .pull-left[ <img src="1.12-slides_files/figure-html/unnamed-chunk-18-1.png" width="504" style="display: block; margin: auto;" /> ] .pull-right[ - **Short Run**: model firm as a price-searching monopolist: - `\(q^*\)`: where `\(\color{purple}{MR(q)}=\color{red}{MC(q)}\)` - `\(p^*\)`: at .blue[market demand] for `\(q^*\)` ] --- # Monopolistic Competition Model: Short Run .pull-left[ <img src="1.12-slides_files/figure-html/unnamed-chunk-19-1.png" width="504" style="display: block; margin: auto;" /> ] .pull-right[ - **Short Run**: model firm as a price-searching monopolist: - `\(q^*\)`: where `\(\color{purple}{MR(q)}=\color{red}{MC(q)}\)` - `\(p^*\)`: at .blue[market demand] for `\(q^*\)` - Earns `\(\color{green}{\pi} = [\color{blue}{p^*}-\color{orange}{AC(q^*)}]q^*\)` ] --- # Monopolistic Competition Model: Long Run .pull-left[ <img src="1.12-slides_files/figure-html/unnamed-chunk-20-1.png" width="504" style="display: block; margin: auto;" /> ] .pull-right[ - **Long Run**: market becomes competitive (**no barriers to entry!**) - `\(\color{green}{\pi > 0}\)` attracts **entry** into industry ] --- # Monopolistic Competition Model: Long Run .pull-left[ <img src="1.12-slides_files/figure-html/unnamed-chunk-21-1.png" width="504" style="display: block; margin: auto;" /> ] .pull-right[ - **Long Run**: market becomes competitive (**no barriers to entry!**) - `\(\color{green}{\pi > 0}\)` attracts **entry** into industry - .blue[Residual demand] for each firm’s product: - **decreases** (more output by other firms) - become more **elastic** (more substitutes from new competitors) - until... ] --- # Monopolistic Competition Model: Long Run .pull-left[ <img src="1.12-slides_files/figure-html/unnamed-chunk-22-1.png" width="504" style="display: block; margin: auto;" /> .tiny[<sup>.magenta[†]</sup> Note it is *not* at the *minimum* of AC(q)!] ] .pull-right[ - **Long Run**: market becomes competitive (**no barriers to entry!**) - `\(\color{green}{\pi > 0}\)` attracts **entry** into industry - .blue[Residual demand] for each firm’s product: - **decreases** (more output by other firms) - become more **elastic** (more substitutes from new competitors) - .hi-purple[Long run equilibrium]: firms earn `\(\color{green}{\pi=0}\)` where `\(\color{blue}{p}=\color{orange}{AC(q)}\)` ] --- # Monopolistic Competition vs. Perfect Competition .pull-left[ <img src="1.12-slides_files/figure-html/unnamed-chunk-23-1.png" width="504" style="display: block; margin: auto;" /> ] .pull-right[ .smaller[ - .hi[Perfect competition] `\((q_c, p_c)\)` - `\(q_c\)` where `\(\color{blue}{P}=\color{red}{MC(q)}\)` - `\(\color{blue}{p_c} = \color{orange}{AC(q)_{min}}\)`, .hi-orange[productively efficient] - Production at lowest average cost - `\(\color{blue}{p_c} = \color{red}{MC(q)}\)`, .hi-purple[allocatively efficient] - Production until .blue[MB] = .red[MC] - Maximum .blue[consumer surplus] (and .red[producer surplus]) - No **DWL** ]] --- # Monopolistic Competition vs. Perfect Competition .pull-left[ <img src="1.12-slides_files/figure-html/unnamed-chunk-24-1.png" width="504" style="display: block; margin: auto;" /> ] .pull-right[ .smaller[ - .hi[Monopolistic competition] `\((q_m, p_m)\)` - `\(q_c > q_m\)`, where `\(\color{purple}{MR(q)}=\color{red}{MC(q)}\)` - `\(\color{blue}{p_m} = \color{orange}{AC(q)}\)` - but not `\(\color{orange}{AC_{min}}\)`, so some .hi-orange[productive .ul[inefficiency]] - `\(\color{blue}{p_m} > \color{red}{MC(q)}\)`, .hi-purple[allocative .ul[inefficiency]] - Less .blue[Consumer Surplus] - Some **Deadweight loss** ] ] --- # Monopolistic Competition vs. Perfect Competition .pull-left[ <img src="1.12-slides_files/figure-html/unnamed-chunk-25-1.png" width="504" style="display: block; margin: auto;" /> ] .pull-right[ - Like a monopoly, produces less `\(q\)` at a higher `\(p\)` than competition, some **DWL** - But like perfect competition, still **no `\(\pi\)` in the long run**! - Outcome is *between* perfect competition & monopoly in terms of efficiency & social welfare ] --- # Monopolistic Competition in Autarky .pull-left[ - Keep it simply, assume `\(MC(q)=0\)` - In autarky, long-run equilibrium for firm is `\(p=AC\)`, `\(\pi=0\)` at `\(q_1, p_1\)` ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-26-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Monopolistic Competition with Trade: Short-Run .pull-left[ - Firm opens up to international trade, has two effects on demand for firm: - greater demand for firm’s products - more competition from other countries’ firms - overall, demand becomes .b[more elastic] ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-27-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Monopolistic Competition with Trade: Short-Run .pull-left[ - Firm opens up to international trade, has two effects on demand for firm: - greater demand for firm’s products - more competition from other countries’ firms - overall, demand becomes .b[more elastic] - Allows firm to lower price, produce more at `\(q_2, p_2\)` and earn some .hi-green[profit] ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-28-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Monopolistic Competition with Trade: Short-Run .pull-left[ - Firm opens up to international trade, has two effects on demand for firm: - greater demand for firm’s products - more competition from other countries’ firms - overall, demand becomes .b[more elastic] - Allows firm to lower price, produce more at `\(q_2, p_2\)` and earn some .hi-green[profit] ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-29-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Monopolistic Competition with Trade: Long-Run .pull-left[ - In reality, the size of the world market (.blue[Home]+.red[Foreign]) has not changed - Thus, not all firms can expand and survive in global market - As all firms try to expand and compete, this .b[lowers demand] for each individual firm ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-30-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Monopolistic Competition with Trade: Long-Run .pull-left[ - In reality, the size of the world market (.blue[Home]+.red[Foreign]) has not changed - Thus, not all firms can expand and survive in global market - As all firms try to expand and compete, this .b[lowers demand] for each individual firm - This continues until new equilibrium, where `\(p=AC\)`, `\(\pi=0\)` again, at `\(q_3, p_3\)` ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-31-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Monopolistic Competition with Trade: Long-Run .pull-left[ - In reality, the size of the world market (.blue[Home]+.red[Foreign]) has not changed - Thus, not all firms can expand and survive in global market - As all firms try to expand and compete, this .b[lowers demand] for each individual firm - This continues until new equilibrium, where `\(p=AC\)`, `\(\pi=0\)` again, at `\(q_3, p_3\)` ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-32-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Monopolistic Competition with Trade: Long-Run .pull-left[ - In autarky (before trade), suppose there were `\(2n\)` firms `\((n\)` in each country) - When trade opens, each firm tries to gain larger share (but not all can) - Some firms exit; firms that remain will produce more than before `\((q_1 \rightarrow q_3)\)` - With trade, and after the shakeout, there are `\(n^\star\)` firms, `\(n < n^\star < 2n\)` - Price & AC fall, and product variety in each country rises from `\(n \rightarrow n^*\)` ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-33-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Monopolistic Competition with Trade: Long-Run .pull-left[ .smallest[ - Which firms will survive and which will exit the market? - Compare two firms, one with .red[high costs], `\(\color{red}{MC_H}\)` and one with .orange[low costs] `\(\color{orange}{MC_L}\)` - .orange[Low cost firm] earns more .hi-green[profits] than .red[high cost firm] - Opening up trade increases competition, lowering profits - .orange[Low cost firms] better equipped to survive falling profits - .red[High cost firms] leave the market; allowing .orange[low cost firms] to expand output! ] ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-34-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Monopolistic Competition with Trade: Productivity .pull-left[ - With fewer firms, the remaining .orange[(low cost)] firms can further increase their output - Exploit economies of scale, moving down their average cost curves - Implies lower costs, lower prices, and greater productivity for the incumbent firms remaining ] .pull-right[ <img src="1.12-slides_files/figure-html/unnamed-chunk-35-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Trade Agreements and Firm Productivity .center[  .smallest[After Canadian free trade agreement with U.S., Canadian productivity increased rapidly by 8.4%, a huge increase over a short time period. Note this is a logarithmic scale!] ] --- # What is at Stake in Competing Trade Theories? .pull-left[ - H-O theory vs. increasing returns - Ex ante vs. ex post comparative advantage - Emphasize different causes of trade - Imply very different policies - free trade vs. industrial policy? - Cultural/aesthetic views of the world? Difference vs. sameness? ] .pull-right[ .center[   ] ]